Why Today’s Mortgage Debt Isn’t a Sign of a Housing Market Crash

Worried about a housing bubble? Let’s unpack the facts:

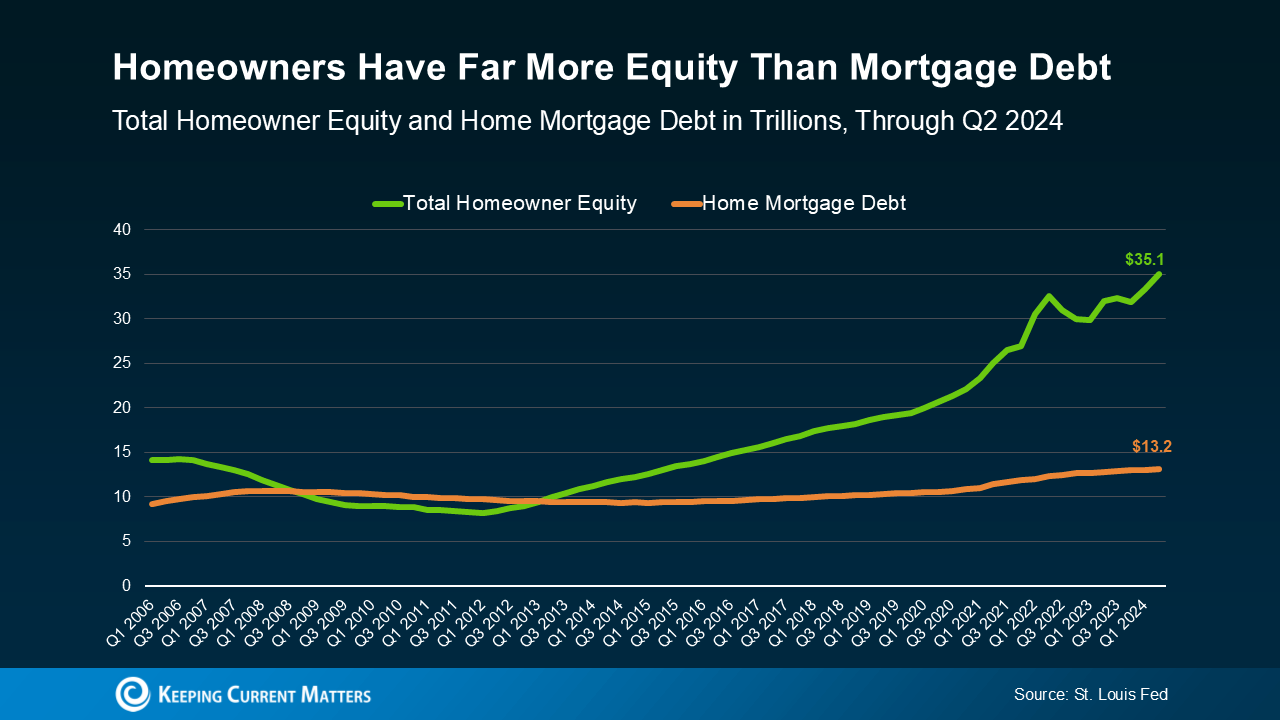

Mortgage Debt vs. Equity

According to the St. Louis Fed, total homeowner equity is $35.1 trillion, nearly three times higher than total mortgage debt at $13.2 trillion. This cushion provides stability in the market.

Late Payments Are Rare

The NY Fed reports that mortgage payments more than 90 days late are still near historic lows. Unlike the 2008 crisis, today’s homeowners are managing their payments well.

Fewer Foreclosures

Marina Walsh from the Mortgage Bankers Association explains:

“Servicers are helping at-risk homeowners avoid foreclosures through loan workout options that can mitigate temporary distress.”

This proactive approach keeps homeowners in their homes and prevents a surge in distressed sales.

Expert Insights

Housing Analyst Bill McBride sums it up:

“There will not be a huge wave of distressed sales as happened following the housing bubble.”

Market Trends

October Existing Home Sales rose nearly 3% year-over-year, the first increase in over three years. Inventories are up 19.1%, giving buyers more options, while home completions jumped 17% in the past year.

The Bottom Line

With high homeowner equity, fewer late payments, and proactive foreclosure prevention, the housing market remains stable. If you’re thinking about buying or selling, the data shows we’re in a strong, resilient market.

Let’s connect to discuss what this means for you!